CS-466/566: Math for AI

Module 01: MinMax Optimization

2026-03-23

Where Are We Now?

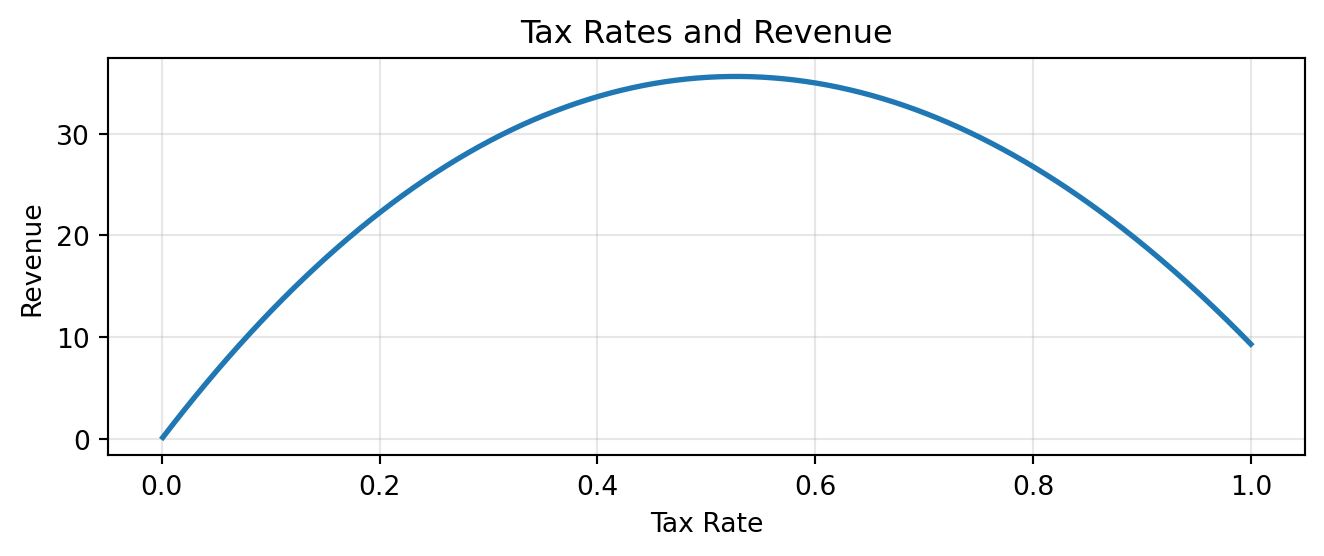

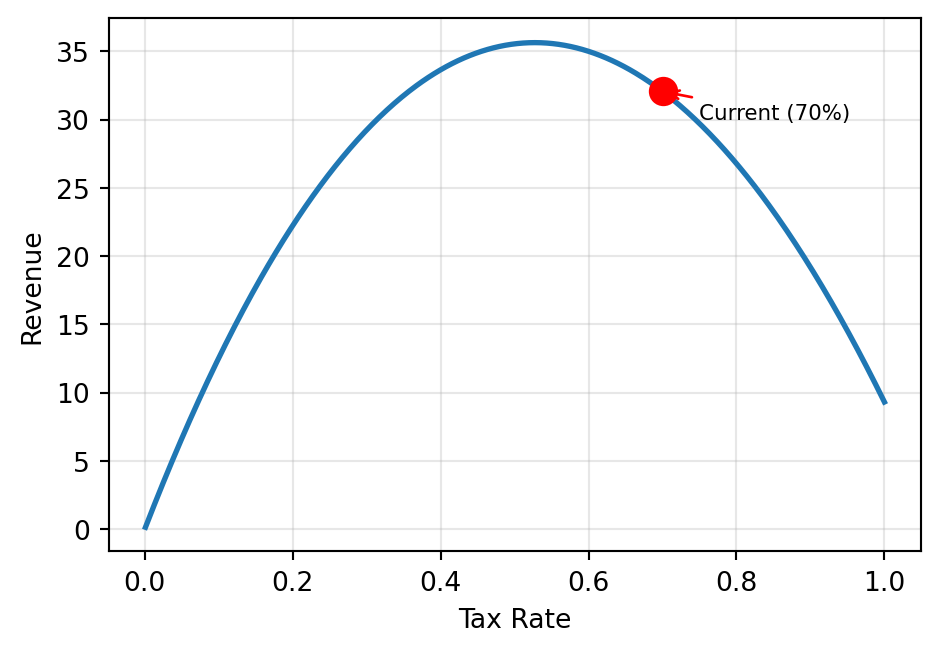

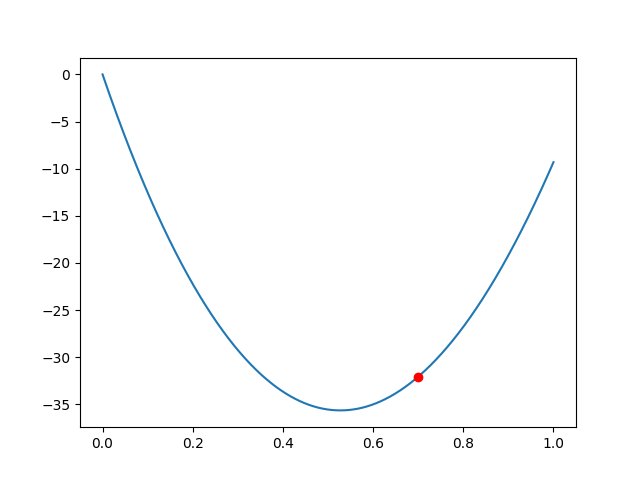

Your country currently has a 70% flat tax. Is this optimal?

current_rate = 0.7

xs = np.linspace(0.001, 1, 500)

ys = [revenue(x) for x in xs]

fig, ax = plt.subplots(figsize=(5, 3.5))

ax.plot(xs, ys, linewidth=2)

ax.plot(current_rate,

revenue(current_rate),

'ro', markersize=10)

ax.annotate('Current (70%)',

xy=(current_rate,

revenue(current_rate)),

xytext=(0.75, 30), fontsize=8,

arrowprops=dict(arrowstyle='->',

color='red'))

ax.set_xlabel('Tax Rate')

ax.set_ylabel('Revenue')

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()We need a precise answer — not just a guess from the plot!

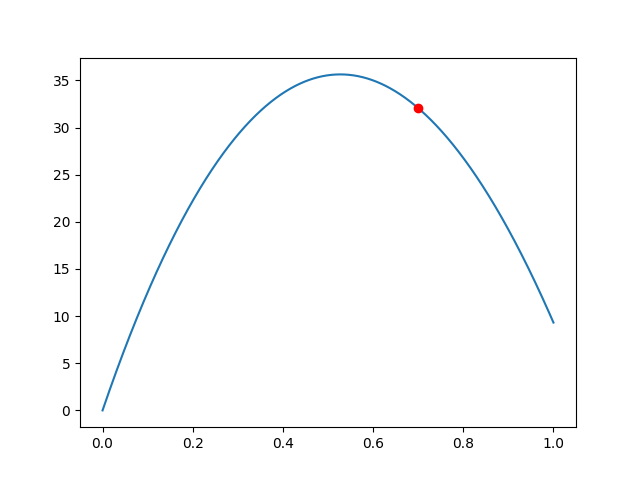

What Does the Derivative Sign Tell Us?

Negative derivative at the red point:

→ Function is going downhill

→ To increase \(f\), move left (decrease \(x\))

Positive derivative at the red point:

→ Function is going uphill

→ To increase \(f\), move right (increase \(x\))

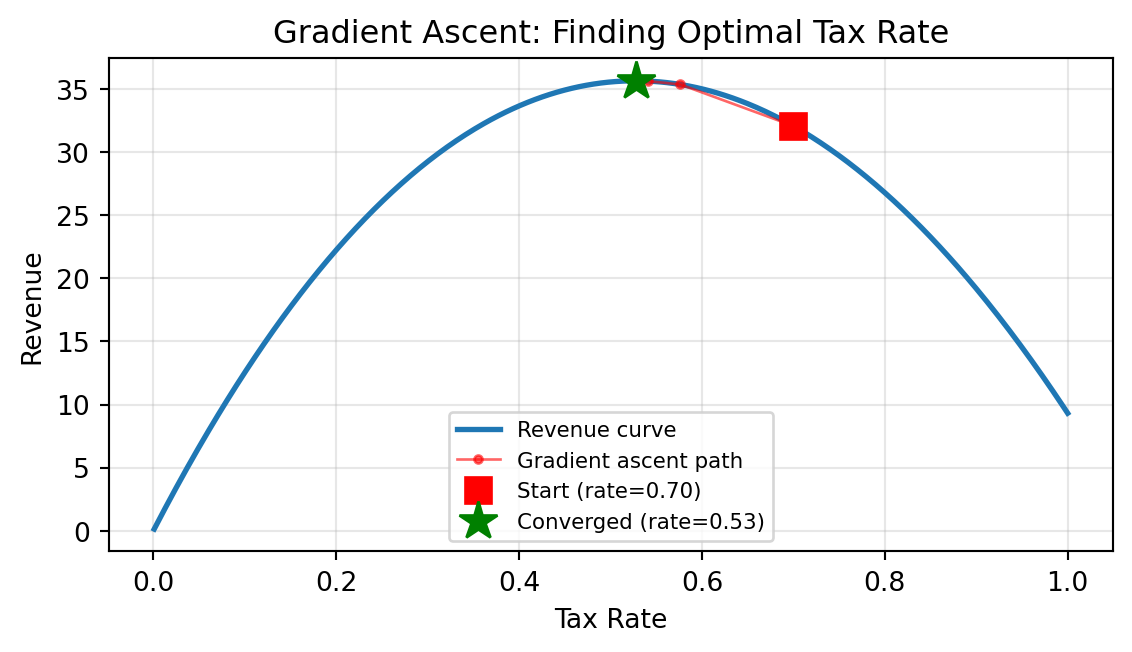

Visualizing Gradient Ascent

Starting from 70%, gradient ascent converges to the optimal tax rate in a few dozen steps.

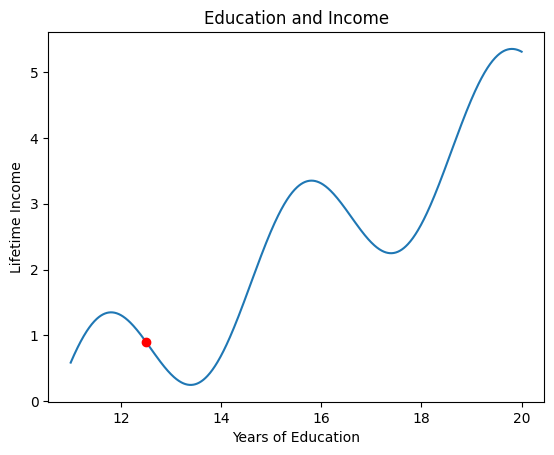

Education and Income: A Real-World Analogy

The Trap of Local Optima:

- Dropping out of school gives immediate income

- But staying in school → higher long-term earnings

- You must temporarily decrease income to reach the global maximum

Gradient ascent is greedy — it can’t see the bigger picture.

Thank You!